[A reader, far more observant than this blogger, pointed out significant items in the documents related to the Sanghvi debacles that the blogger overlooked in an earlier post. This reader posted the text below as a comment, but the observations deserved a wider audience, so I have included them here. I also have included the documents referred to in the piece.]

On The Audit

- [A source has told me that she had another job lined up and gave two weeks’ notice. This only furthers the narrative of how Sanghvi has alienated her employees] Why would an employee retire after 29 years and a couple months? There are extra longevity benefits to retiring at 30 years, which increases the pension amount. Why not wait another 10 months? It’s common to retire at 20, 25, or 30 years because each milestone has an extra benefit. This alone raises doubts about an immediate resignation or earlier retirement than planned. The Director of Finance would understand better than anyone the benefit of reaching the 30-year milestone. It must have been so bad that forgoing personal financial gain was less important than the value of escaping the working environment in the Finance department under Sanghvi.

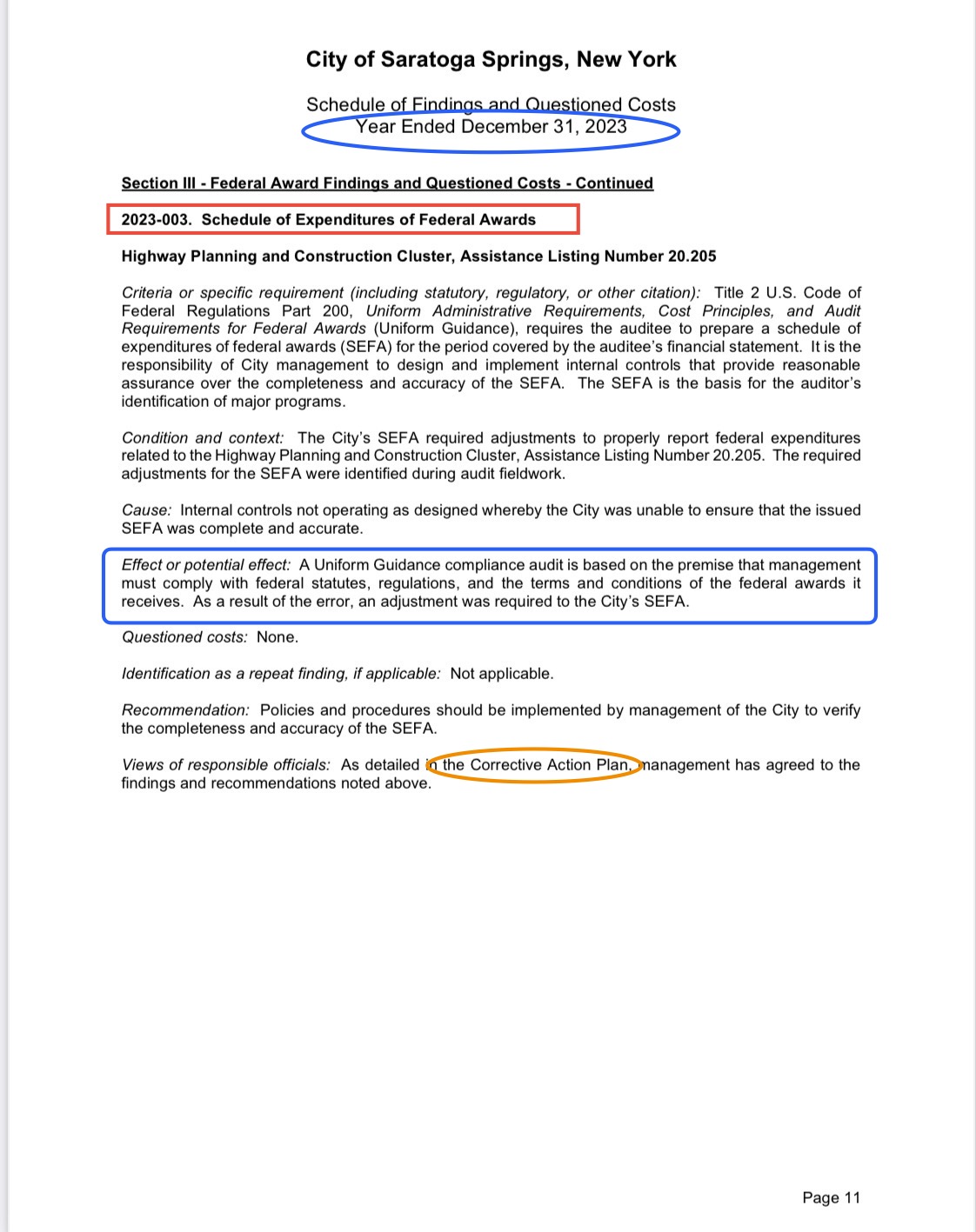

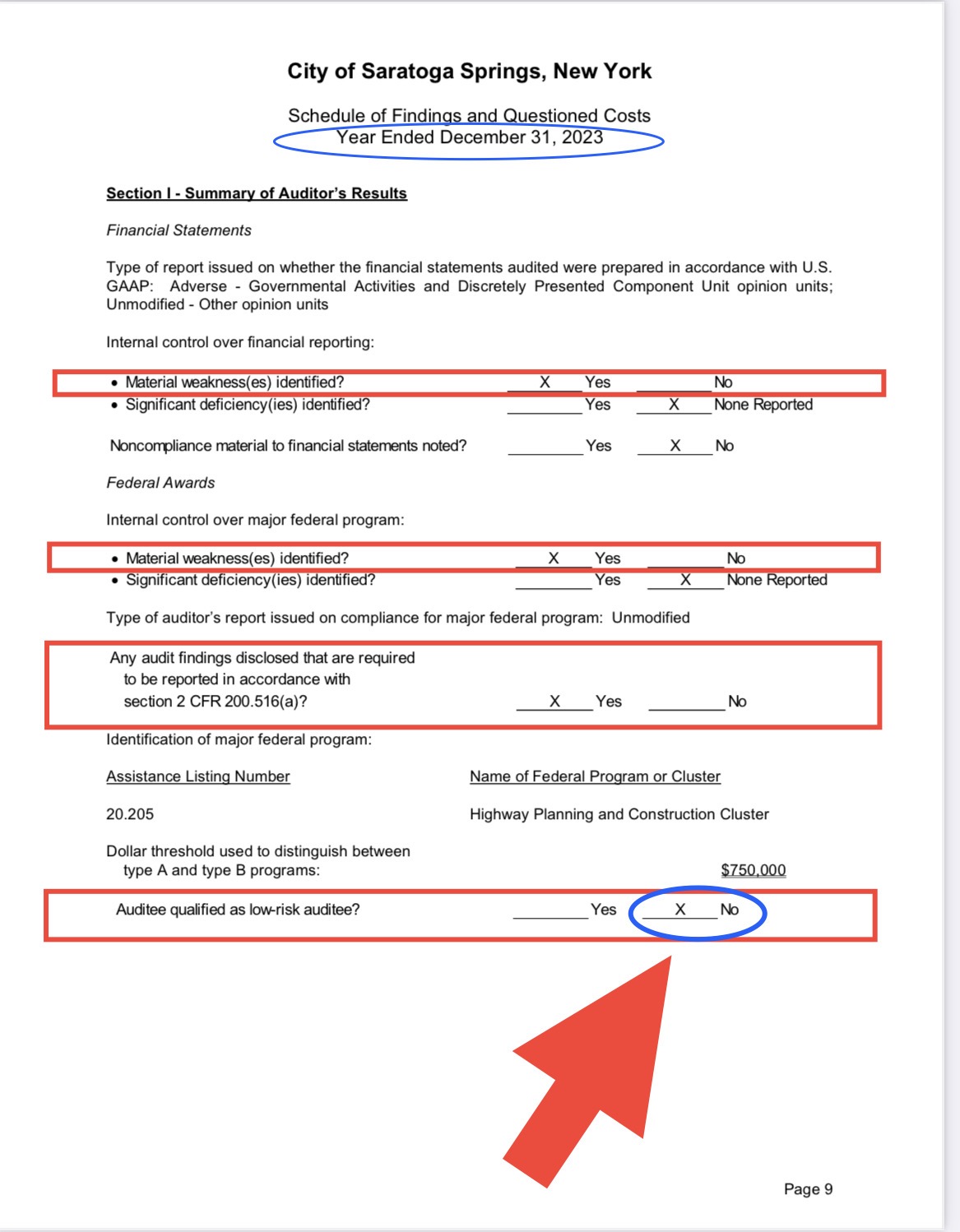

- The independent annual finance audit documents in this post [JK: my earlier post] are only the tip of the iceberg. In looking further into this report, it’s Sanghvi’s worst yet. Each year, her leadership has proven a decline in competence and increase in violations to the degree that Sanghvi was required to create three corrective action plans for three violations as a result of the most recent audit. Each year, she had to create at least one corrective action plan per audit.

- These corrective action plans require Sanghvi to explain why the violations occurred, how she plans to correct them, and a timeline for correction. She also signs as the responsible party for these violations. She failed to satisfy her plan from the 2022 year-end audit, hence the repeat offense you posted from the 2023 year-end audit.

- She consistently cites vacancies and increased training and supervision as the reason. This is another red flag. Why can’t she keep employees? There seems to be a pattern suggesting a lack of planning and effort to fill or prevent vacancies. When audits find an adverse opinion of her ability to run the department, you would think she would work very hard to do a better job. The most recent audit proves that she didn’t get the message that she needed to improve significantly.

- Anyone who cannot responsibly handle taxpayer money should not be the Commissioner of Finance.

- This blog post highlights the areas in which the public needs to demand further scrutiny. Keep investigating.

- Maybe it’s time for Sanghvi to leave politics. It seems she could benefit from self-reflection. Maybe reading self-help books to support growth in her ability to take accountability for her failures and acceptance of her need to improve would be helpful. She might consider hiring a life coach to work on learning interpersonal communication and interaction skills and help her develop empathy for others.

- Mr. Kaufmann, please further investigate and post the corrective action plans or provide a link to the audit so that the public can see just how badly she is handling taxpayers’ money.

The Documents

The following documents were part of the audit published in the earlier post.

This document requires the city to submit an action plan to address the problems uncovered by the audits. It is alarming that this 2023 audit includes the fact that Sanghvi’s action plan, committed to responding to problems with the 2022 audit, was never carried out and is included again with this 2023 audit, with a due date of December 31, 2025, for its completion.

Section III states:

- “The City did not obtain an independent audit with[in] the required period for submission.”

- “…purported inaccuracies of capital asset balances.”

- “The city should develop a course of action to ensure that future single audit reports are completed and submitted…”